Are you curious about how accounting software actually works behind the scenes? Understanding the process of accounting software can transform the way you manage your finances and save you hours of tedious work.

Whether you’re a small business owner or just looking to streamline your accounting tasks, knowing each step helps you make smarter decisions and avoid costly mistakes. You’ll discover the clear, step-by-step process accounting software follows to keep your financial records accurate, organized, and up to date.

Ready to take control of your accounting like a pro? Keep reading to unlock the secrets of how accounting software simplifies your financial world.

Key Features Of Accounting Software

Accounting software simplifies financial management by combining key features into one tool. These features help track money, organize data, and create financial reports. They save time and reduce errors in managing accounts. Understanding these core features reveals how accounting software supports business efficiency and accuracy.

Transaction Recording Modules

Transaction recording modules store all financial activities. They cover sales, purchases, payments, and receipts. Each entry updates accounts automatically, keeping records accurate. These modules ensure every transaction is logged and categorized. This process helps maintain clear and complete financial data.

Automation And Bank Integration

Automation reduces manual work by handling routine tasks. It can schedule payments, send invoices, and update ledgers automatically. Bank integration links software directly with bank accounts. This feature imports bank transactions in real time. It helps match payments and receipts quickly and accurately.

Report Generation

Report generation creates summaries of financial data. Users can produce balance sheets, profit and loss statements, and cash flow reports. These reports provide insights into business health. They help owners and managers make better decisions. Reports are customizable to fit different business needs.

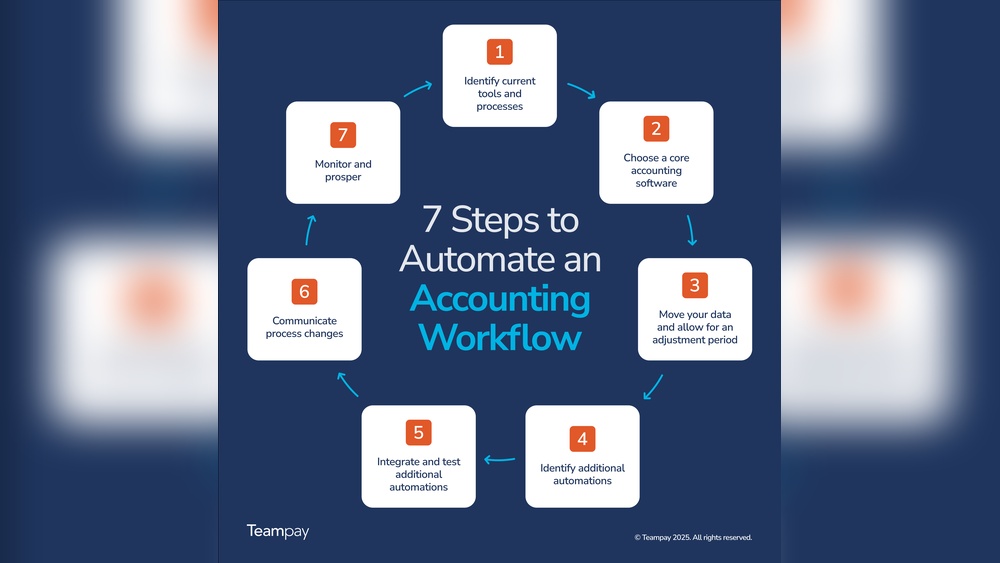

.png "What is the Process of Accounting Software? Step-by-Step Guide 1")

Credit: www.teampay.co

Setting Up Accounting Software

Setting up accounting software is a vital first step in managing business finances efficiently. It involves entering basic information and customizing the system to fit your company’s needs. Proper setup helps track financial data accurately and saves time later.

The setup process includes configuring company details, organizing accounts, and assigning user roles. Each step ensures the software runs smoothly and securely. Let’s explore these key parts in detail.

Configuring Company Details

Start by entering your company’s name, address, and contact information. Choose the correct fiscal year and currency for your business. This information forms the foundation of your accounting records. It also ensures reports and tax filings are accurate.

Set your tax rates and payment terms next. These settings automate calculations and reminders. They reduce errors and keep your business compliant with tax laws.

Chart Of Accounts Setup

The chart of accounts is a list of all accounts used to organize financial transactions. It includes assets, liabilities, income, and expenses. Customize this list based on your business type and size.

Create accounts that match your financial activities. Group similar accounts to simplify reporting. A well-structured chart of accounts helps track money flow clearly.

User Roles And Permissions

Assign roles to control who can access and change financial data. Common roles include admin, accountant, and viewer. Setting permissions protects sensitive information and reduces mistakes.

Limit access based on job responsibility. For example, sales staff may not need access to payroll data. Proper user management supports security and accountability.

Entering Financial Transactions

Entering financial transactions is a key step in using accounting software. It involves recording all money-related activities accurately. This ensures that the financial data stays organized and reliable. Proper entry of transactions helps businesses track income, expenses, and other financial movements effectively. Each transaction must be logged with clear details to maintain accuracy.

The process covers various areas such as sales, purchases, and payroll. Each area has its own set of records and steps. Using accounting software simplifies this by automating many tasks. It reduces errors and saves time for business owners and accountants alike.

Sales And Invoices

Sales transactions begin with creating invoices. Invoices show what a customer owes for goods or services. Accounting software allows quick entry of these invoices. It records the date, amount, and customer details. The software tracks payments against these invoices. This helps monitor which invoices are paid or still open.

Automated reminders can be sent to customers for overdue payments. This keeps cash flow steady. Sales data also updates the accounts receivable balance automatically. This way, businesses always know how much money they expect to receive.

Purchases And Bills

Purchases involve buying goods or services from suppliers. Bills received from suppliers must be entered into the software. Each bill includes details like vendor name, date, and amount due. The software records these bills as accounts payable.

Tracking bills helps businesses know what they owe and when to pay. Many accounting programs allow attaching scanned copies of bills. This keeps all documents in one place. Payment schedules can be managed to avoid late fees.

Payroll Processing

Payroll processing is entering employee salary and wage details. It covers hours worked, taxes, and deductions. Accounting software calculates net pay automatically. It also records payroll expenses in the accounts.

Proper payroll entry ensures employees are paid correctly and on time. The software generates pay slips and tax forms. This simplifies compliance with tax laws. Payroll data integrates with financial reports for a full view of business costs.

Credit: www.conceptdraw.com

Managing Accounts Payable And Receivable

Managing accounts payable and receivable is a key part of accounting software. It helps businesses keep track of money they owe and money they will receive. This process ensures smooth cash flow and accurate financial records. Clear steps guide users through handling payments and invoices efficiently.

Vendor Setup And Approval

First, vendors must be added to the system. Their details, like name and contact, are entered. The software checks for duplicates to avoid errors. Approval is needed before vendors can be used. This step controls who the company pays and protects against fraud.

Invoice Matching And Approval Workflow

Invoices received from vendors are matched with purchase orders. This confirms the goods or services were ordered and received. The software routes invoices to managers for approval. Only approved invoices move forward for payment. This step prevents incorrect or duplicate payments.

Payment Processing And Verification

Payments are processed based on approved invoices. The system schedules payments according to terms set with vendors. Bank details are verified to ensure correct transfers. After payment, confirmation is recorded in the software. This step keeps records accurate and helps avoid late fees.

Reconciliation And Adjustments

Reconciliation and adjustments are key steps in accounting software. They ensure financial data is accurate and reliable. This process helps identify differences between records and correct them promptly. Regular reconciliation keeps accounts balanced and trustworthy.

Adjustments are necessary to update records for errors or changes. They maintain the accuracy of financial statements. Without these steps, businesses might face incorrect reports and financial issues.

Bank Statement Reconciliation

Bank statement reconciliation compares the company’s records with the bank’s statement. It helps find mismatches in deposits, withdrawals, or fees. This step ensures all transactions are recorded correctly. It prevents fraud and errors from going unnoticed. Reconciliation is usually done monthly for best results.

Error Detection And Correction

Accounting software detects errors automatically during reconciliation. It highlights missing entries or incorrect amounts. Users can review these errors and make corrections quickly. Correcting errors avoids future financial problems. This process improves the trustworthiness of financial data.

Adjusting Journal Entries

Adjusting journal entries update the ledger for any changes or corrections. These entries fix errors found during reconciliation or reflect accruals and deferrals. They ensure financial statements show the true financial position. Adjustments might include prepaid expenses, depreciation, or unrecorded liabilities. Proper adjusting entries keep accounting records complete and accurate.

Closing Books And Reporting

Closing books and reporting mark the final step in the accounting software process. This phase ensures all financial data is accurate and complete. It prepares the business for analysis, tax filing, and decision-making. The process involves organizing data, verifying balances, and generating key reports.

Trial Balance Preparation

The trial balance lists all ledger accounts with their balances. It helps verify that total debits equal total credits. Accounting software automatically compiles this list from recorded transactions. Accountants review the trial balance to spot errors or unusual entries. Fixing these issues early prevents problems in financial reports.

Financial Statement Generation

Financial statements summarize the company’s financial health. Common reports include the income statement, balance sheet, and cash flow statement. Accounting software uses trial balance data to create these reports. These statements help owners, investors, and regulators understand business performance. They also guide future planning and budgeting.

Year-end Closing Procedures

Year-end closing finalizes accounts for the fiscal year. It involves adjusting entries, closing temporary accounts, and resetting balances. Accounting software automates many closing tasks to save time and reduce mistakes. Proper year-end closing ensures the new year starts with clean, accurate books. This process supports smooth audits and compliance with legal requirements.

Best Practices For Smooth Operation

Ensuring smooth operation of accounting software requires following certain best practices. These help keep financial data reliable and processes efficient. Proper habits reduce errors and save time. They also support compliance and secure information.

Focus on key areas like data accuracy, internal controls, and timely updates. These steps build a strong foundation for your accounting system.

Maintaining Data Accuracy

Accurate data is the heart of accounting software. Enter all information carefully and double-check entries. Use clear naming and consistent formats for accounts and transactions.

Regularly reconcile accounts to catch mistakes early. Train staff to understand the importance of precise data. Accurate records support better decisions and reporting.

Implementing Controls And Audits

Set up controls to limit access to sensitive data. Use role-based permissions to prevent unauthorized changes. Keep logs of all actions within the software for review.

Schedule regular audits to examine data integrity and compliance. Audits help spot fraud or errors before they grow. They also ensure policies are followed correctly.

Regular Software Updates

Keep your accounting software up to date with the latest versions. Updates fix bugs, improve security, and add useful features. Check for updates often and apply them promptly.

Test updates on a backup system before full deployment. This avoids disruptions and data loss. Staying current ensures smooth performance and protection against threats.

Credit: jfwaccountingservices.cpa

Frequently Asked Questions

What Are The 7 Steps In The Accounting Process?

The 7 steps in the accounting process are: identify transactions, record journal entries, post to ledger, prepare trial balance, adjust entries, close books, and generate financial statements.

How Do Accounting Softwares Work?

Accounting software records financial transactions, organizes data into modules like invoices and payroll, and generates reports. It automates calculations and tracks expenses to simplify bookkeeping and improve accuracy. Users input data, and the software processes it to maintain real-time financial records and support decision-making.

What Are The 5 Processes Of Accounting?

The five accounting processes are: identifying transactions, recording journal entries, posting to ledger, preparing trial balance, and generating financial statements.

What Is Accounting Software?

Accounting software automates recording, managing, and reporting financial transactions. It simplifies tasks like invoicing, payroll, and bookkeeping for businesses.

Conclusion

Accounting software simplifies managing financial data step by step. It records transactions, tracks payments, and generates reports clearly. This process helps businesses stay organized and save time. Using accounting software reduces errors and improves accuracy in bookkeeping. Small business owners can better understand their finances with easy-to-use tools.

Overall, accounting software supports smooth financial management and decision-making. Choose the right software that fits your business needs and skills. Regular use keeps your accounts updated and reliable. The process may seem complex, but consistent practice makes it easier.